Christmas has come early, thanks to the BCSC not being happy with the disclosure in the original Nov 20th PR (link), Garibaldi, issued a new press releases clarifying the information from the first 4 drill-holes at Nickel Mountain (link).

Summary

High-grade mineralization restricted to narrow zones

Massive Sulfide zones are very narrow, maximum thickness 1.5m (Hole EL-17-03)

Discovery Zone Massive Sulfides - appears to be a small pod, adjacent holes didn't intersect it.

We get a table with hole locations and a breakdown of the assays!

Massive sulfide intervals highlight in red

I've highlighted the massive sulfide intervals (** in the press release table). However, in the Nov 20th PR, we are told that:

In the table, this isn't labelled as a massive sulfide zone, is this just a typo? I'm splitting hairs, but we often see in other deposits we often see S.H.I.T. intervals related to veinlets/pods of mineralization.

We are still missing a decent plan map, but with the information provided I've brought the data into 3D (get the viewer file* from here - link), and due to my prodigious use of a ruler, I've also added the EL-17-14 discovery zone as as well.

*you'll need to download the latest version of Leapfrog viewer (4.1) from here (link)

Plan View

1 square = 50m

There are a lot of holes in a small area, and the Discovery Zone is very close to the narrow Ni-Cu intercepts in holes EL-17-02 and 04.

Section View

Nickel

EL-17-14 sulfide zone is Black

Copper

EL-17-14 sulfide zone in black

Again we see that the Discovery sulfide body is surrounded by drill-holes. Does this mean that it is very small?

The Discovery zone is only 32m from hole EL-17-04 and 27m from EL-17-02. However, it isn't completely close off, there is potential to expand it to the north and east, unlike the other zones where adjacent holes hit virtually nothing.

I'll be updating the model with more data as if it is released.

I might as well jump onto the Garibaldi-bashing wagon. I had stood on the edge muttering to myself, how the feck are were they worth >$400M based on feck all?

Their website is shite, devoid of information and looks like it was created by a child, probably the same one who created the 'fact sheet', but at last we got a section through the Nickel Mountain, the first decent 'image' from the project....ever (link)

It is a shame that it wasn't accompanied by a plan map, which would be useful in showing the 14 Garibaldi holes and the location of the 1960s drilling?

When looking at a map/section - start with the basics

Scale - look to see if there is a grid or scale bar.

Quickly see how far apart the holes are located (50-100m)

How 'big' the massive sulfides are

Legend - this tells you the colors used for grades and rock types

check out the dark grey = no assay = Nothing of interest (i.e. no sulfides) in the core

How consistent is the mineralization - does it link up between adjacent holes?

No, we get a few scratchy hits, with a small disseminated halo.

You need to ask yourself, can I, armed with a mighty No. 2 pencil (HB in the normal parts of the world), join the zones together?

here is an easy one for Garibaldi to do

I'm not an expert on Nickel deposits, but I've decided to annotate it, to highlight some interesting features and I've made a few observations.

So, how big are our massive sulfides?

They are soooooooo massive, that each one has just been hit 1 hole. Approximate dimensions:

Big Boi - reamed by hole EL17-14 = 29m x 12m

Old MoFo - penetrated by hole EL-17-03 = 2m x 91m

Skinny Man - pricked by hole EL17-04 = 5m x 50m

So we have 3 small, inconsistent massive sulfide bodies, with minor disseminated sulfide halos.

So, after a disappointing press release, how can you save face, well, we needs to ask the FAG.

Hello FAG* here, I was disappointed that Garibaldi were defeated by unseasonable Northern Canadian weather. Who would have thought that they would have had snow this time of year in the Polar Riviera. (*Fraudulent Angry Geologist) I was very disappointed with Garibaldi's program, a true professional would have moved holes EL17-01 approx. 20m to the left, that would have hit >100m of disseminated sulfides, but they redeemed themselves with Hole EL17-14. So, if you are a company like Garibaldi, dedicated to not releasing any useful information, my advice is, have some fun, and really do to town on the drilling. Here is my idea:

Proposed holes in GREEN

Those 4 holes are beauts, multiple sulfide hits and nice and easy. OK, you're drilling the same areas 2-3 times, but we are searching for 'geological continuity' not drilling for resources. Chuck in a few words like, structural complexity, offsets and everyone will be happy and you'll get some decent hits to keep the shareholders happy. If those dipshit geologists keep bleating, remember that with all that cash you raised, you can keep giving yourself a huge salary for the next 3-4 years, which is a happy thought.

Just a note to Dorian Leslie - your maps are great.

In between PRs about awesome drill results we got this one (link) showing some results from their regional exploration on their Machos-Florida Santa Cruz-La Hueca concessions in Southern Ecuador.

Dear SolGold - the La Alumbrera Mine is Miocene in age (~7Ma), not Jurassic (145-201Ma). So they don't get any cool dinosaurs (e.g. Chilesaurus (link), just Terror Birds, and check your scale bars, they are wrong.

Summary

Good address - large property package located in the Jurassic porphyry/epithermal belt in Southern Ecuador (Mirador and FDN)

Good initial results - Regional sampling has identified 3 areas of interest

Follow-up rock-chip sampling identified an initial area with good indications of porphyry mineralization.

So it is early days, but SolGold have hit the ground hard, applied a logical exploration strategy when working on a large property. Start big, do regional sampling to identify areas of interest, and then focus on them.

Location, location, location

As I've mentioned before, porphyry/epithermal deposits occur along belts, and in Ecuador there are 2 principal belts:

Older Jurassic Belt - hosts Fruta del Norte (14Moz Au) and Mirador (890Mt @ 0.56% Cu and 0.16 g/t Au)

Younger Miocene Belt - hosts Cascabel, Junin etc.

So, if you are looking for these types of deposits, these areas are where you want to be, and SolGold's concessions are located in the Jurassic belt. They have acquired a large property (~25km x 10km), and unlike many exploration companies, have actually conducted a logical exploration program to quickly evaluate the property and identify areas of interest for follow-up work.

Stream sediment sampling

This is used to quickly evaluate large areas to identify areas of interest for follow-up with more detailed sampling. The idea is that if a deposit is exposed at surface, it will be eroded and indicator minerals (gold, magnetite etc.) will go into the silt, sand and clay in a stream or river bed.

Each one of these horrendously colored polygons is a drainage basin

SolGold have collected 180 stream sediment samples, probably 1-2 per basin, that have identified 3 principal Areas of Interest (AOIs).

2 small and a biggie, the red outlines are highlighting core areas (I think)

Just from collecting 180 samples, we can see that >80% of the property appears to have a low potential to host porphyry Cu-Au mineralization. This probably costs SolGold ~ US$20K, and has identified 3 areas of interest where more detailed (i.e. more expensive, more time consuming) exploration can be conducted.

The key is to identify areas with potential and not get distracted by the areas without. This is very unfashionable as a typical Junior exploration company will simply amalgamate concessions and do nothing with them.

Prospecting and sampling

After you have defined your AOIs, now you have to visit them to see what you've got, and it is this basic prospecting (i.e. looking for evidence for mineralization) that we are given in this PR.

Now, before you all go weak at the knees at the assays and photos, let's take a step back. SolGold have told us that they have ~470 rock chip samples, but this PR is only giving us info from just 46 samples (~10%), why? Are these:

The greatest hits?

The 1st batch, with more results to come?

It is obviously the former, figure 3 in the PR tells us that in the other areas they sampled disseminated chalcopyrite with low grade copper gold mineralization.

We are also told that there is biotite alteration, this is typically found in the (potassic) core of a porphyry system, and it can be a bit of a double-edge sword, as this is where you typically get the highest grades. This is also characterized by the presence of bornite. However, if the samples collected from this area are not very high-grade, is this an indication that the porphyries are not well mineralized? This is a rhetorical question as it can only be answered by the truth machine (the drill-rig).

mineralization, but if these samples aren't very high-grade, this may indicate that the mineralization

We can also see where these samples have come from, they are shown on the map above, but why don't we zoom in a bit.

Left = Copper; right = Gold, the red circle is 1.2 km wide

We see a cluster of samples, some nice high-grade ones, but the majority are low grade, which isn't unexpected at this stage.You also have to remember that most rock-chip sampling is biased, the pretty rocks get sampled first, so they aren't really representative of the overall grade of the rocks.

So it is a good start from SolGold, they have identified an interesting target with decent initial results. At this stage all you should be reading into this press release is that SolGold have found evidence for porphyry-style copper gold mineralization on their new concessions. It is a good start and I hope to see more information from SolGold on their regional exploration activities.

I took a quick look at Pretium's Q3 financial report (link). They made a small loss (net $7m), but this is because they weren't able to sell all of their gold (produced 82,203 ounces Au, sold 55,413 ounces).

However, I'm more interested in the underlying performance of the mine and how quickly it will ramp up to the production figures outlined in the 2014 Feasibility study.

Reserves

lots of gold at a good grade as well...

Their annual production breakdown, for head grade by year

They should be mining material grading 13-16 g/t Au

A typical chart - quick ramp up, in the good stuff for the majority of the project life, then a big drop as they run out of reserves.

Before everyone sends me heaps of abuse (feel free to do so), I understand that we are very early in the mine life, and but I want people to look at the underlying performance at Brucejack.

In the Q3 financials

Head grade = 10.5 g/t Au

Throughput = 2,840 tonnes per day

Recovery = 96.5%

In the 2014 Feasibility Study

Head grade (life of mine) = 14.1 g/t Au

Throughput = 2,700 tonnes per day

Life of mine recovery = 94%

Plant ramp up = good

Recoveries = excellent

Head grade = poor - head grade is ~33% lower than planned.

I know this is very boring, for Brucejack has occasionally raised a number of questions regarding the quality of its resources, the geology and its ability to support a large underground operation. I was surprised that the head grade reported in the Q3 financials was so low. There are a number of factors, including:

Still in the ramp up stage and not yet reached the >15 g/t Au areas?

Excessive dilution, mining barren country rock with the gold veins

Inconsistent gold grades (large variability over very short distances)

For me, it will be interesting to see how the head-grade evolves over time. Will Pretium be back on track in the Q4 financials, or is that an indicator for potential problems in the future with the project not quite reaching the production and profitability figures as promised?

DISCLOSURE: I own shares in Sol Gold, and before you ask, I'm irritated that they did a financing at GBP0.25p.

Well we are moving into the home straight, we've been promised a maiden resource by the end of the year (link), so it was nice to get some more drill results to have a look at. You can download my 3D model here (link) and open it in Leapfrog Viewer.

Obviously, we are all waiting for the initial resource calculation that was promised by the end of the year. We've only got a couple of weeks before the Christmas party and tax sell-off season starts, so it will be interesting to see if SolGold can deliver.

Summary

Infill holes, duplicating and extending to depth known mineralization

Is hole CSD-17-028 hinting at a core of a system just to the south (currently being explored by hole 030)?

Hole CSD-17-026-D1

Similar grades to adjacent hole CSD-14-009

high-grade lower zone (from 1150m) looks to be quite consistent

upper zone looks to be quite narrow, and may link up with the high-grade zone in hole 14

Hole CSD-17-028 - drilled between holes 021 and 022, similar grades and thicknesses

Geology Drivel

Even though these results are groundbreaking, just extending and exploring known zones, they do appear to show that in there could be more than one grade center at Alpala. I also hate that they don't highlight where the holes are located.

I not going to say that there are 2 porphyry centers (I haven't seen the drill-core or any interpretative geological plans for the project), so I've done some doodling on the map that accompanied the PR.

WARNING: Geology doodles by an insane, de-bearded geologist

So I'm quite excited about holes 30 and 30-D1. If they come back with some decent intercepts my stupid idea alternate interpretation could be correct, it could have a nice positive effect on an undated resource calculation in 2018, as these holes won't have been completed by the time the initial 43-101 resource is published in the next few weeks.

If we look at the holes individually, and again, I only have the data in the press release to work with, so it is incomplete and a best guess.

Hole CSD-17-026-D1

We can see that hole 026-D1 hit a decent zone of material grading >0.7% Au and >0.45 Cu. My feeling on why the Au zone appears thicker is a effect on how the data has been reported, and we would see a >1g/t zone from 1400m to 1550m but it wasn't split out in the PR.

Hole CSD-17-028

Hole CSD-17-028 was drilled between holes CSD-16-021 and 022, so I'm assuming that it was an infill hole to provide more confidence in these intercepts. It returned very similar results to hole 021.

Resources

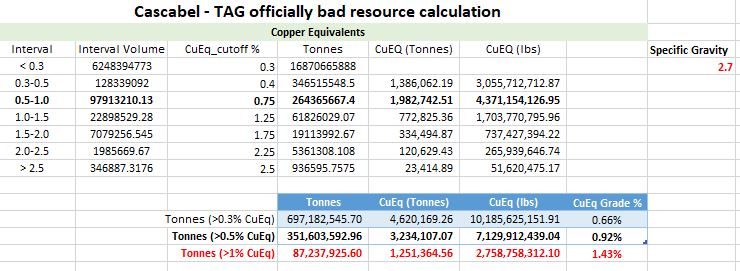

I've hidden this at the bottom of the post. I'm not 100% (or even 50%) confident in my officially bad resource guesswork for Alpala, but I wanted to include the table to see what numbers I come up with to see how SolGold will get to their:

I regard this statement as a BS, the recent drilling didn't do much to their resources, and I don't know why they are mentioning that they want to define a billion tonnes at 0.9% CuEq at a 0.3% CuEq cutoff. That puts it firmly in the uneconomic category for an underground block-cave.

So according to Macquarie, for a 0.9% CuEq block cave to give an IRR of 15%, it will need to have Cu at >US$3.5/lb and Au >$1750/oz.

Personally, I'll be looking at the size and continuity of the >1% CuEq cutoff resources.

So, I'm not sure that they'll get to their billion tonnes, but I'm convinced that my model is under reporting the narrow-high-grade zones.

Vizcachitas, the "Largest Independent Copper Project in the Americas" we are told by Los Andes. All that is missing is "undeveloped", to really tell us how great the project is!

All projects are great from afar.....

Summary

A large, but low grade resource and with a very small 'high-grade' zone.

Good recoveries, but minimal by-product contribution

>95% for Copper

55-70% for Mo

Expansion of near surface resources looks limited, but hole V2017-10 did intersect some interesting grades at depth.

Bad geography, located in the bottom of a relatively steep valley, this could have big implications on strip ratios as minor changes in pit slope angle may mean moving very large amounts of waste rock.

2014 PEA show that a small (40 ktpd) operation is very marginal and that very minor (5%) increases in CAPEX or OPEX will have a major impact on the project economics.

So, Vizcachitas is too small, too low grade with marginal economics. As they say, can't make a silk purse out of a sow's ear.

*resources haven't been updated to include the 2015-17 drilling.

Geo-babble

DISCLOSURE: I've compiled as much of the information as possible that is in the public domain. However, I've had to estimate the angle of dip, and I'm sure that I've only been able to find summarized assay data for ~65% of the 'deposit'.

You can download the Leapfrog project from here (link)

Resources

The first area I wanted to look at is the quality of the resources, especially the tonnage at high, medium and low cut-off grades.

lots of high-grade, just not in the resources....

So we can see that the majority of the deposit is very low grade, and a small part (only 19%) of the indicated resources scraping over 0.5% Cu.

However, the recent drill results have been interesting (link) with some (reported) thick, reasonable grade intercepts, but we need to check where these holes have been drilled (link).

You can quickly see that the majority of the new holes are clustered in areas of known mineralization, with a couple, including hole V2017-10 drilled to the north.

In the image below I have created a >0.4% Cu grade shell for the project using (left) pre-2015 drilling and (right) all drilling. To see how the resource has changed.

changes circled in red

There is a new area to the north, centered on hole V2017-10 and some minor expansion around the edges of the known mineralization. There are no new high -grade zones, and when you look at it, the >0.4% Cu grade shell is quite poddy and doesn't form a nice solid consistent zone with a high-grade core.

Here are some sections, you'll notice that the >0.4% Cu zone doesn't extend to great depths.

Section 2800N

Section 3400N

Section 3900N

These zones aren't very thick, but we can see that the mineralization in Hole V2017-10 is open in several directions, but is deep, all other mineralized zones appear to have been close off or are very narrow, so unfortunately, I can't see much exploration upside.

Development

There are rumors that Los Andes want to re-market Vizcachitas as a small (40,000 tonnes per day), high grade deposit, and we are fortunate that a financial analysis of a 44,000 tpd operation was include in the 2014 PEA.

I mean, I like the fact that they are so modest, a discounted NPV of just US$3 million is quite cute when compared to other large copper projects, and a leisurely payback period of a decade, I mean why make money quickly, when you can make it slowly and savor it.

I mean look at the numbers, all the best projects, like Livengood's epic 2013 PEA, you have a positive IRR and a negative (discounted) NPV.

It is going to be a lot of fun developing such a marginal project, where any minor increase in CAPEX or OPEX with rape you up the ass. Personally, I can't think of any mining project that has every gone over budget or not completed on time.

One the cross sections above I put on the surface trace. It shows that the mineralization is found at the bottom of a steep valley, that Los Andes loves to take photos of:

a river runs through it..

So, it is a bit hilly, has a river than runs through the project (that hopefully isn't a water source for any urban centers), so another factor that will impact the economics of the project is the pit slope angle. Back in 1999, Golder estimated a 42-47 degree angle, and I've doodled it on the best section, along with steeper and gentler angles

You can see how much additional rock (grading less than 0.4% Cu) needs to be moved.

The same will happen if you decide to mine the deeper resources, as you go deeper you needs to move more and more low-grade waste rock on either side of the deposit.

So, after all of this blathering, you can see that the project simply isn't good enough, the economics are crap, and just a minor change in CAPEX, OPEX, metal prices, rock quality and stability can conspire to wreck it. The recent exploration data hasn't shown any upside, just a single hole that hit some medium grade mineralization at depth.